Every treasurer knows what FX options are – but not necessarily how to use them to maximum effect. This article examines the challenges hedgers face when using options, including costs, and outlines the optimisation opportunities that can be harnessed by moving away from conventional buy-and-hold FX strategies.

The FX market remains the largest market in the world. According to the Bank for International Settlements’ (BIS’) most recent triennial report (published in 2022), average daily volume in the market across all products is pegged at $7.5tr.[1]. Of that gargantuan amount, FX options may represent a small slice at $300bn[2], but that still makes the FX options market the largest options market by far. For comparison, equity options in the US trade, on average, a daily dollar volume of $20bn[3].

Even in the fixed-income markets, the best estimate of global daily volumes for options runs to $40bn[4] across all currencies. The takeaway is that despite options representing just 4% of total FX volumes, the absolute amount of activity is large and liquidity available, at least in the major currencies, is typically quite deep.

With that as a backdrop, the question at hand is how best for hedgers to utilise FX options as part of their hedging programmes. The most frequent complaint about options from a hedger’s perspective is their cost. This relatively high cost stems from the fact that there is an opportunity available for option owners during the life of the option that does not exist in the FX forward space.

The initial premium cost of the option includes payment for this opportunity. Therefore, to utilise FX options most effectively as a hedge, the hedging entity must recognise this opportunity and take advantage of those times when it makes economic sense to manage, or adjust, the position. This is the opposite of the more common buy-and-hold strategy.

In fact, the theoretical basis of an option’s value is subject to the amount of time between the execution and the expiration as well as the expected amount of volatility in the underlying product. And that cost can add up, especially for longer-dated options. Hedge tenors of one year or 18 months can result in option premia of 5% of the notional value of the hedge or more depending on the implied volatility of a given currency pair. Given that investment, active management would seem to be worthwhile.

So, how can corporate hedgers best take advantage of options when managing their FX exposures? This article will give an overview of the way options work and then introduce a framework that offers a more systematic approach to managing option positions to achieve predefined goals by relying on the market’s underlying movement rather than treasury staff opinions or market views. In a second article, this framework will be modified to work with zero-premium collars, a popular hedging structure.

Options 101

An option is a contract that offers the purchaser the right, but not the obligation, to either buy (call option) or sell (put option) an underlying asset at a specific price (strike price) on a chosen date (expiry date) in the future. The price of any option is determined by five variables, four of which are observable at the time of execution, and the fifth, which is the effective ‘price’ of that option. These variables are:

- Expiration date

- Strike price

- Underlying spot price

- Risk-free interest rate

- Implied volatility

When a corporation seeks to execute an options hedge, they will typically define variables one and two, while the market defines variables three and four. The counterparty bank (it is almost always a bank in corporate FX options) is responsible for determining variable five.

Generally, what happens then is the corporate keeps the option on their books as an offset to some identified exposure and waits for the expiry date to determine if the option ultimately has any value. When purchasing an at-the-money option (an option whose strike price is set at the current market forward), that probability is basically a coin toss. But there is a better way to manage these positions once they have been executed.

An options return framework

Rather than simply waiting for the option to expire, whether in the money or out of the money, a corporate can (and should) take a more active role in managing the exposure. Consider, the potential benefit of an option is that while purchasing protection, if the market moves such that the option falls out of the money, the corporate’s underlying position will improve by an amount greater than the fall in the value of the option. Now, the FX market is famously volatile so the currency in question can easily move both in the money and out of the money during the option’s life. Taking advantage of the times when the option moves out of the money is the key to improving the overall value that a treasury team can add to any corporation.

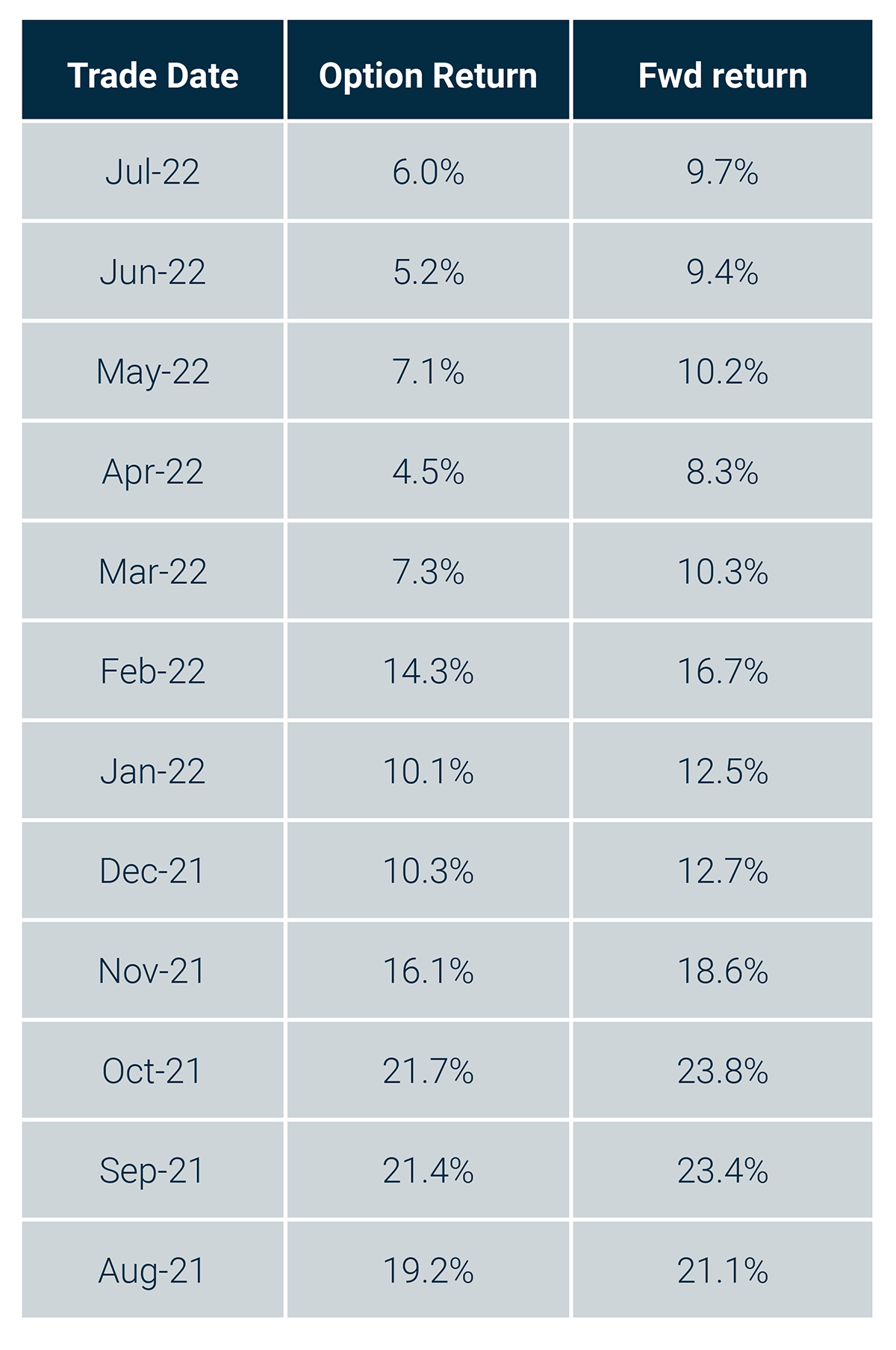

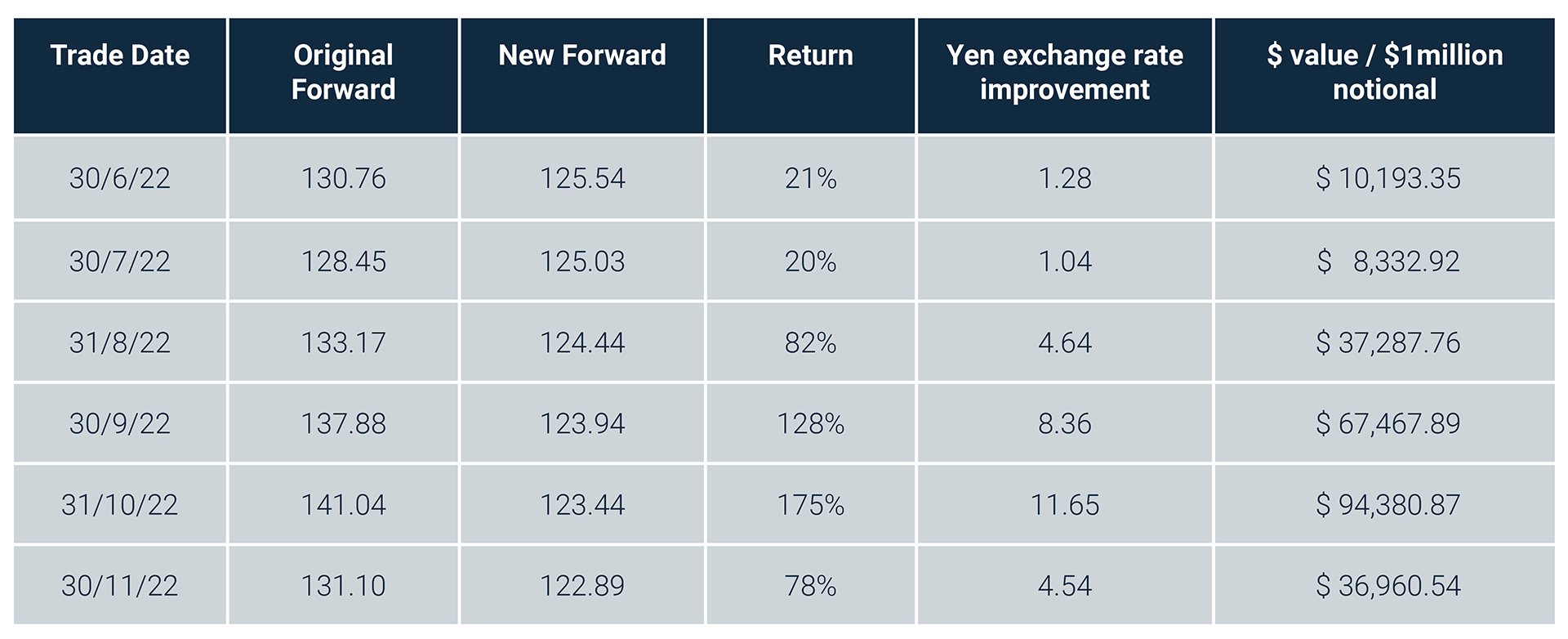

Let us consider an example to better explain this idea (data from Bloomberg, see table 1, below).

Table 1

Data from Bloomberg, calculations by @Fx_poet

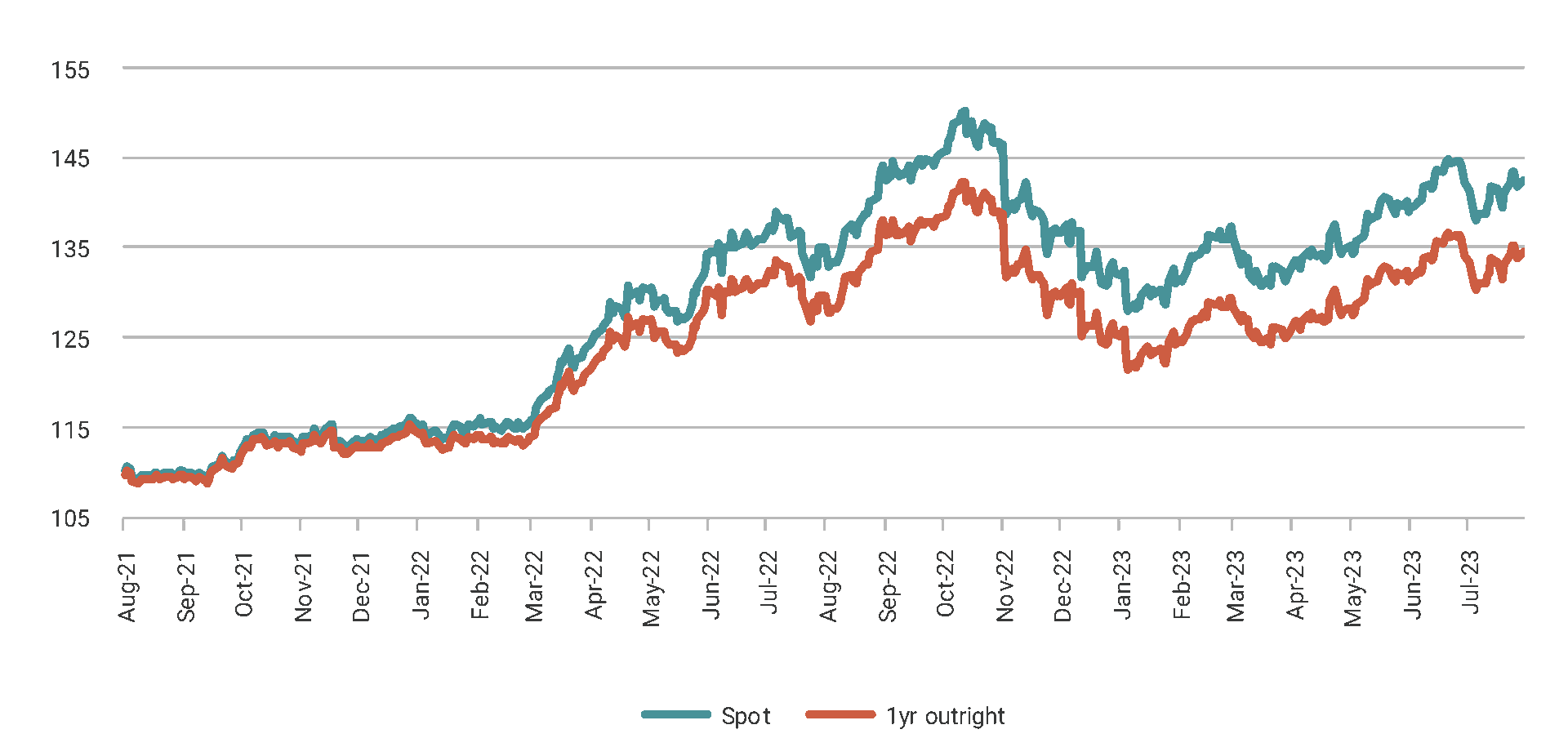

FIG 1: USDJPY Spot and 1-Year Outright Prices

The above chart (figure 1), shows the spot and one-year forward outright movement in USD/JPY for the past two years. From August 2021 to the dollar’s peak in October 2022, the dollar rallied nearly 37%. Then, in the wake of the Bank of Japan intervening to prevent further JPY weakness, the dollar fell back 15% in the ensuing two months. Those are quite substantial moves and since then we have seen the dollar rise sharply yet again. The point is that for corporates with revenues in Japan, the USD value of those revenues would have fallen quite sharply right up until the dollar’s peak in October 2022.

Now, let’s assume that a hypothetical corporation with JPY revenues was operating a hedge programme where they purchased one-year at-the-money forward JPY puts at the end of each month to hedge their forecast revenues. If they held those options to maturity, it would have worked effectively for the first year (see table 1), although as always, given the secular decline in the yen, a simple forward would have had better performance with the difference between the two simply the cost of the premium. As the dollar rose, you can also see how the difference between the two returns widened, which is a direct representation of the rise in implied volatility and correspondingly the size of the premium.

However, starting in August 2022, holding them to maturity may not have been the optimal strategy. Instead, during the dollar’s sharp decline in September and October, the corporate could have sold their options back at a particular point in time and very likely improved their overall hedge outcome. The purpose of this framework is to determine that point in time.

The first step in this process is to rethink how a corporation considers the payment of the option premium. Rather than simply an expense, a different viewpoint would be that it is an investment designed to improve the firm’s overall financial results. From this perspective, it is a natural step to view the potential return on that investment and to set a target for how much return the company would like to earn before unwinding its optionality and fixing the hedge rate at the new, improved market forward. For instance, the company could set a return based on its internal rate of return (IRR) metrics, or some multiple of those metrics. Historically, returns of 30% or more can be achieved, meaning that the improvement in the hedge rate can equate to 30% or more of the premium initially paid.

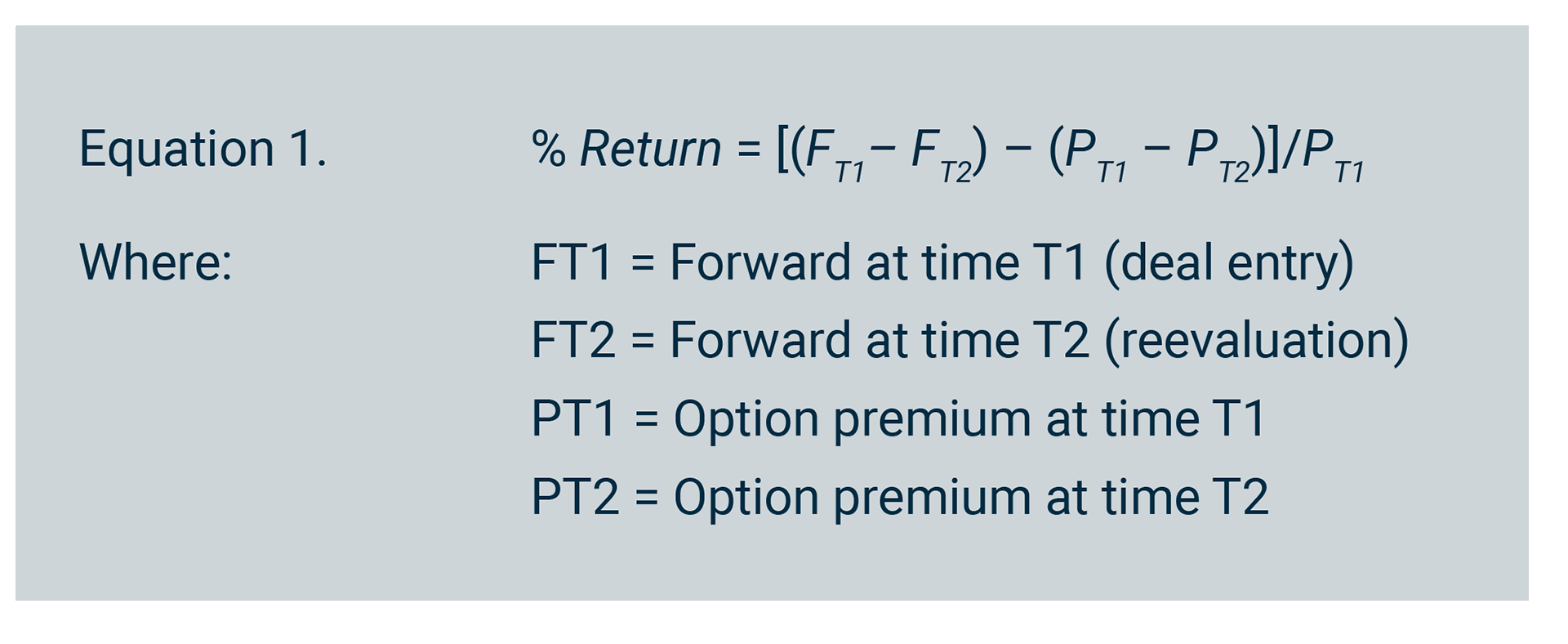

The next step is to calculate that return on a regular basis, via following Equation 1 below, and if the desired return is achieved, the company can adjust its hedge from an option to a forward and lock in that improvement. This hedge conversion should fit within the accounting framework as well by simply de-designating the option hedge and designating the new forward as the hedge.

All we are doing here is comparing the change in both the forward exchange rate and the option premium from the time of the initial deal to the current values. When compared with the initial premium, a return on that premium can be calculated. If, in our case, the dollar falls enough, that return will be greater than the initial premium payment and an indication that unwinding the option and implementing a forward will add value to the overall hedge framework of the company. Experience has shown that a net return of 30% or more is an excellent time to consider adjusting from options to forwards.

Table 2 |

Data from Bloomberg, calculations by @Fx_poet

Working with our USD/JPY example above, calculations show that the value of this strategy became evident in January as the dollar reached its local nadir. Table 2 above shows that there was an opportunity to adjust both the September and October options to forwards and generate excess value for the firm.

These results were based on the lowest point the dollar reached on a closing basis, which implies the exercise must be performed regularly for best results. However, given the simplicity of the calculation, the information for daily calculations should be readily available.

Conclusions

Options offer extraordinary flexibility in a hedging programme but only if they are managed with an eye towards taking advantage of the inherent features of the contract. By reconsidering the premium as an investment, in the case of a purchased option, one can seek to improve overall returns by taking advantage of those times when a large gain can be booked on that premium investment.

History has shown that utilising these techniques can improve overall treasury risk management in a systematic manner. Remember, too, that options on other underlying assets can be viewed and managed in the same way. This is not restricted to the FX world.

Notes

1. https://stats.bis.org/statx/srs/table/d11.1

2. Ibid.

3. https://www.statista.com/statistics/1277648/daily-options-turnover-value-share-exchange-usa/

4. https://stats.bis.org/statx/srs/table/d7?f=pdf